The Portfolio Concentration Debate

It frequently happens that a man delivers his opinions with such boldness and assurance that he appears to be under no apprehension as to the possibility of his being in error. The offer of a bet startles him, and makes him pause. Sometimes it turns out that his persuasion may be valued at a ducat, but not at 10. If it is proposed to stake 10, he immediately becomes aware of the possibility of his being mistaken – Immanuel Kant, The Critique of Pure Reason (quoted in Maria Konnikova The Biggest Bluff, p. 38)

How many stocks should you own in your portfolio?

This is a very important question and there is a great debate between those who believe in a high level of concentration and those who believe in diversification. (Unfortunately, since the field of stock analysis is still young, this subject has not been addressed to the extent one might wish).

Warren Buffett and most of his value investing brethren subscribe to the philosophy of high concentration: “Put all your eggs in one basket and watch that basket closely”.

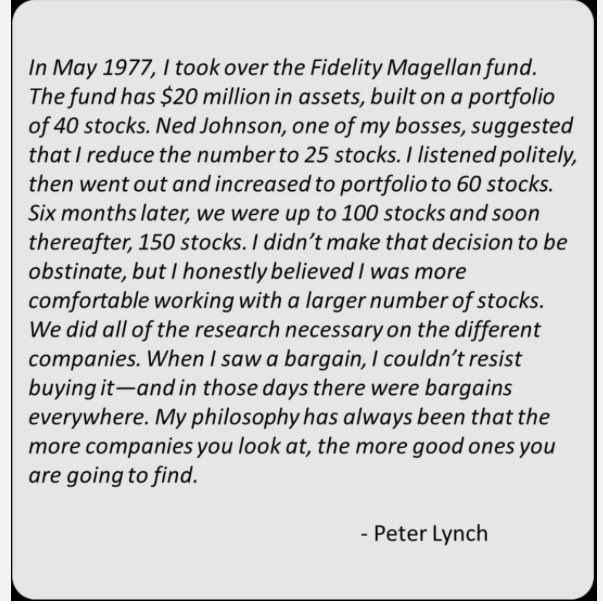

Personally, I like to own a lot of stocks and so I was happy to come across the above quote by Peter Lynch on how he did too.

What are the reasons cited by those recommending concentration?

The first reason is obvious. Why would you dilute your returns by placing money in inferior ideas? If there is a stock you have a lot of conviction in and a stock you have less conviction in, you should put all the money in the former and none in the latter.

The problem arises because all stock picks are essentially predictions about the future or bets. Since the future is unknown, outcomes are always probabilistic. Further, because we’re human, our judgment of probabilities may be incorrect. As a result, even if I have a higher level of conviction in one idea than another, it can often still be prudent to put some money in the idea with lesser though still strong conviction – for the simple reason that I could be wrong about the probabilities.

In other words, diversification respects fallibility: No matter how good you are, you will frequently be wrong about predicting the future. A study of even Warren Buffett’s illustrious career shows many bad investments that he obviously had conviction in at the time.

That’s one reason I personally like to own a lot of stocks and ETFs. While I weight them differently based on my level of conviction, I rarely put more than 4-5% in one stock or 15-20% in one theme because I could be wrong. Stuff I have less though still positive conviction about could work out better because I’m fallible and living in a complex world of imperfect information.

On the other hand, many concentration oriented value investors are known to put 20%, 30% or even more into their best ideas. I’m always impressed, for example, by those who put 20%, 30% or more into Tesla. The position size combined with the difficulty of understanding how that particular stock will turn out is reckless in my opinion. Huge position sizing can sometimes be justified but it’s very risky. You have to have a very high level of skill and conviction to invest this way because if you’re wrong it destroys the performance of your entire portfolio.

The second reason the concentrationists give is limited knowledge. Since human beings are limited in time, energy and knowledge, you can only have real insight into a few things. You can’t know everything about every stock in every industry, much less everything about all the different types of investments: bonds, currencies, options, futures, etc…. Therefore, you should concentrate your bets in the areas where you have real knowledge.

Obviously they have a point. But some people know more about more things than others. Like Peter Lynch said: “The more companies you look at, the more good ones you are going to find.” Different investors read more, work harder on expanding their circle of competence, are willing to try new things, etc… That means that some of them have a wider circle of competence than others i.e. a sphere of investments in which they can have an edge.

Being a polymath like Lynch, I like to think I know a lot about a lot of different areas of the market – though of course what I don’t know dwarfs what I know. As a result, I think I can optimally hold up to 100 securities at a time – whereas the concentrationists usually recommend holding between 10 and 20.

At the end of the day, this debate hinges on principles like imperfect information, complexity, the uncertainty of the future and the fallibility of the human mind. The concentrationists seem to have a lot more confidence in their ideas than I do in mine. In addition, I like to think I have broader knowledge than investors because of my voracious research. As a result, I like to own more securities than they do because I’m less confident in each individual idea and have more ideas.

Where you fall on the spectrum depends on your specific set of skills and liabilities. (Like yesterday’s blog “What To Do When Your Stock Becomes Overvalued”, this blog falls under the category of “Portfolio Management”. Stock picking isn’t just about picking the right stocks but about how you construct a portfolio that best implements your idiosyncratic market insights – as well as the adjustments you make over time as illustrated in yesterday’s blog).

This blog was inspired by reading the chapter “The Birth of a Gambler” in Maria Konnikova’s The Biggest Bluff: How I Learned To Pay Attention, Master Myself and Win. In particular, Konnikova cited the great philosopher Immanuel Kant as proposing betting as the best way to deal with the imperfect information, complexity and uncertainty of the world. That’s because bet sizing reflects the probabilistic nature of outcomes.