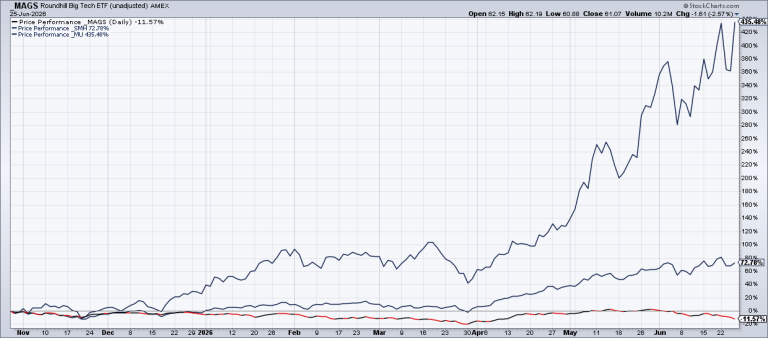

Buy The Dip In Gold

On March 29, 2024 The Wall Street Journal’s Aaron Back wrote a prescient piece about why gold was rallying despite a lack of inflation (“Gold Is Rallying. It Isn’t About Inflation This Time” [SUBSCRIPTION REQUIRED]; I wrote about Back’s article…