CRM Is Not A Growth Stock Anymore

Single digit growth territory is generally where Silicon Valley software companies go to die – or, at least, start paying dividends – Dan Gallagher, “Salesforce Keeps Growth Dreams Alive Enough” [SUBSCRIPTION REQUIRED], WSJ Fri 12/1

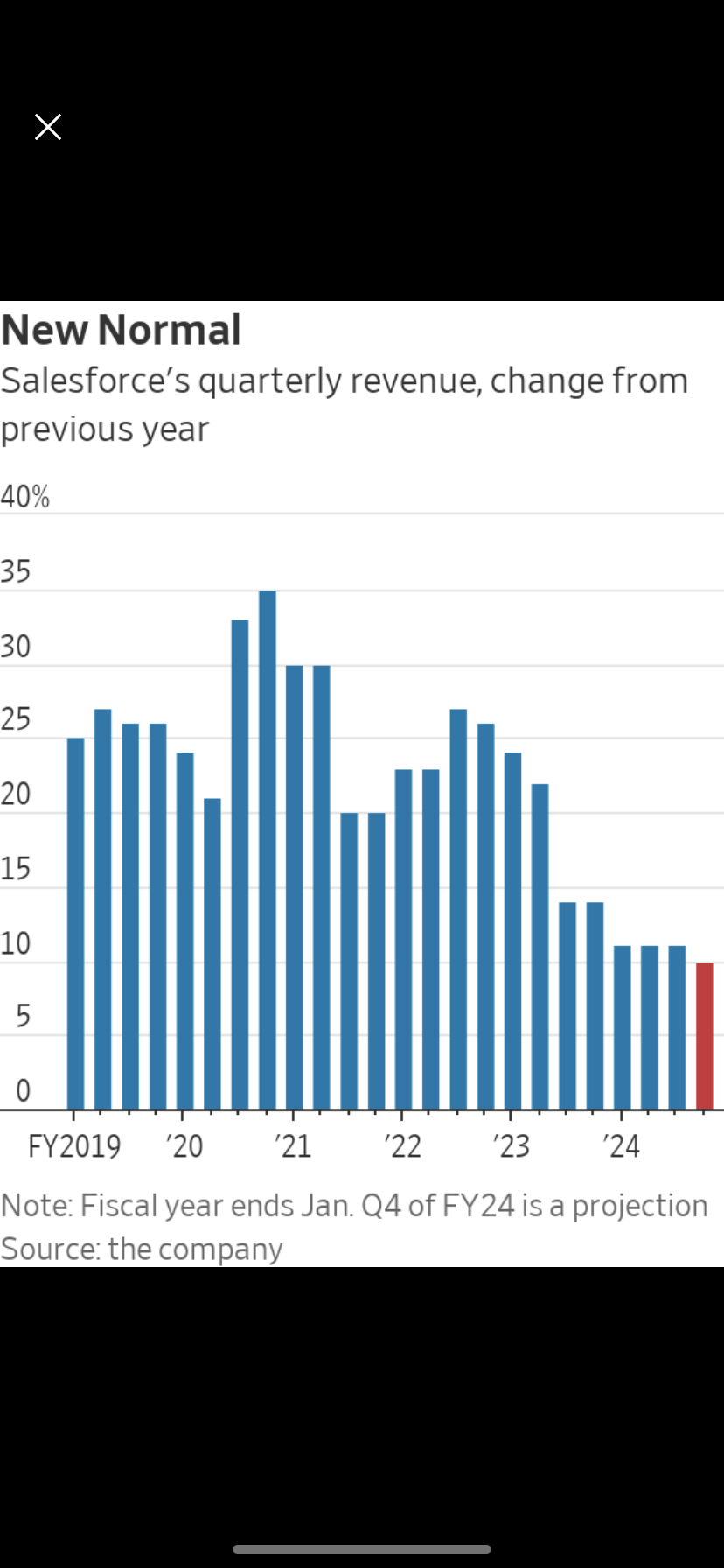

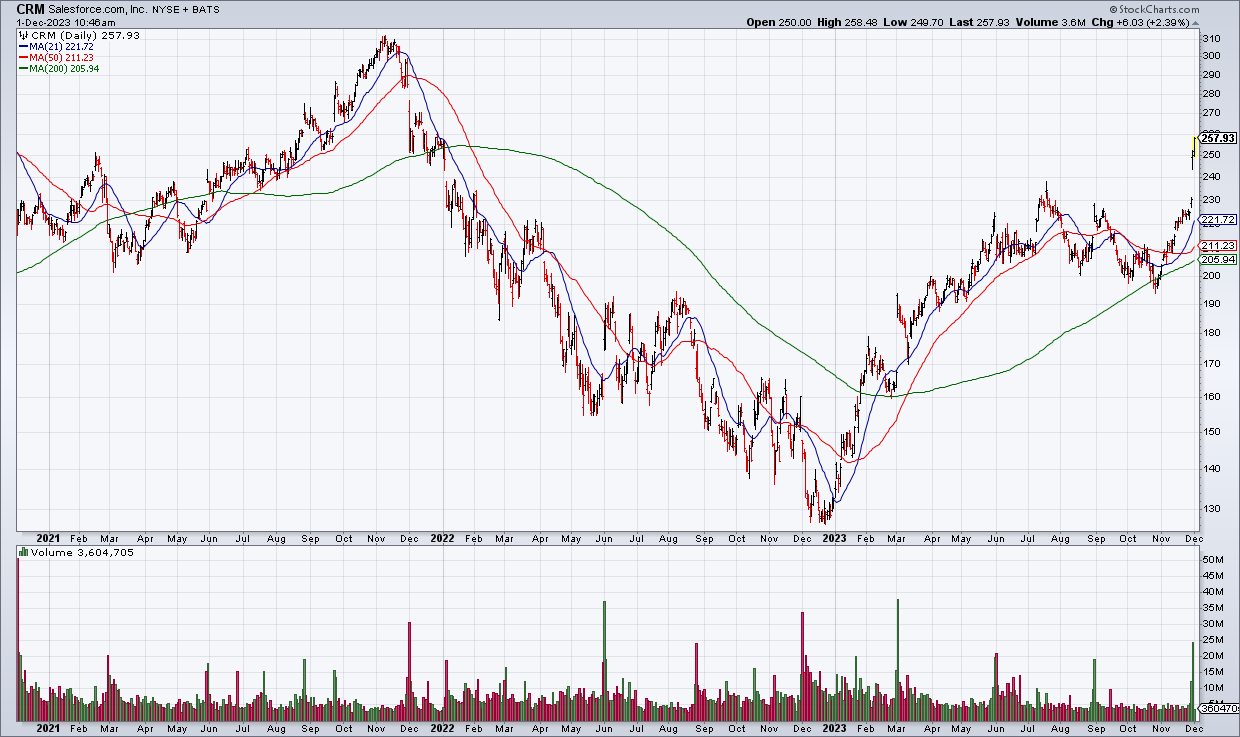

Salesforce (CRM) stock has had a great year and is surging even higher on the back of its latest earnings report released Wednesday afternoon. Call me cranky but I’m not impressed: 10% revenue growth is not sexy! And it doesn’t deserve a 30x multiple.

CRM has propelled the latest leg higher in its stock price by controlling expenses resulting in surging operating margins of over 30%. That’s great. But cutting expenses can only get you so far when growth is slowing. And that’s the other story at CRM: revenue growth guidance for the current quarter amounts to only 10% year over year.

If CRM has squeezed most of the expenses it can out of its operations and margins can’t go any higher, then the stock can’t either because the company isn’t growing the way it used to. It needs to be revalued as a value stock with 20x multiple. That’s my thesis and it’s why I sold some shares short this morning.

Disclosure: Top Gun is short shares of CRM.