In Search Of Deep Value: ZM & AAP

Most of the time cheap stocks are cheap for good reason. While they look good on current financial metrics like the P/E ratio, their businesses are in decline and a more far sighted analysis of their business reveals them to be value traps. Nevertheless, many of us are still attracted to cheap stocks which brings me to the subjects of this blog: Zoom (ZM) and Advanced Auto Parts (AAP).

I have been trying unsuccessfully to pick a bottom in ZM for quite some time now. As I wrote three months ago in “Is ZM A Value Trap?”, while ZM looks good on short term financial metrics the question is the long term health of its business in what appears to be a highly competitive environment. At this stage, ZM has essentially no top line growth though it earns a lot of money and has a fortress balance sheet. As I wrote three months ago, because I don’t know how ZM will fare over the long term and yet I can’t help myself from being interested in the stock, I’m managing risk through a very small position size. ZM reports 2Q23 earnings Monday afternoon.

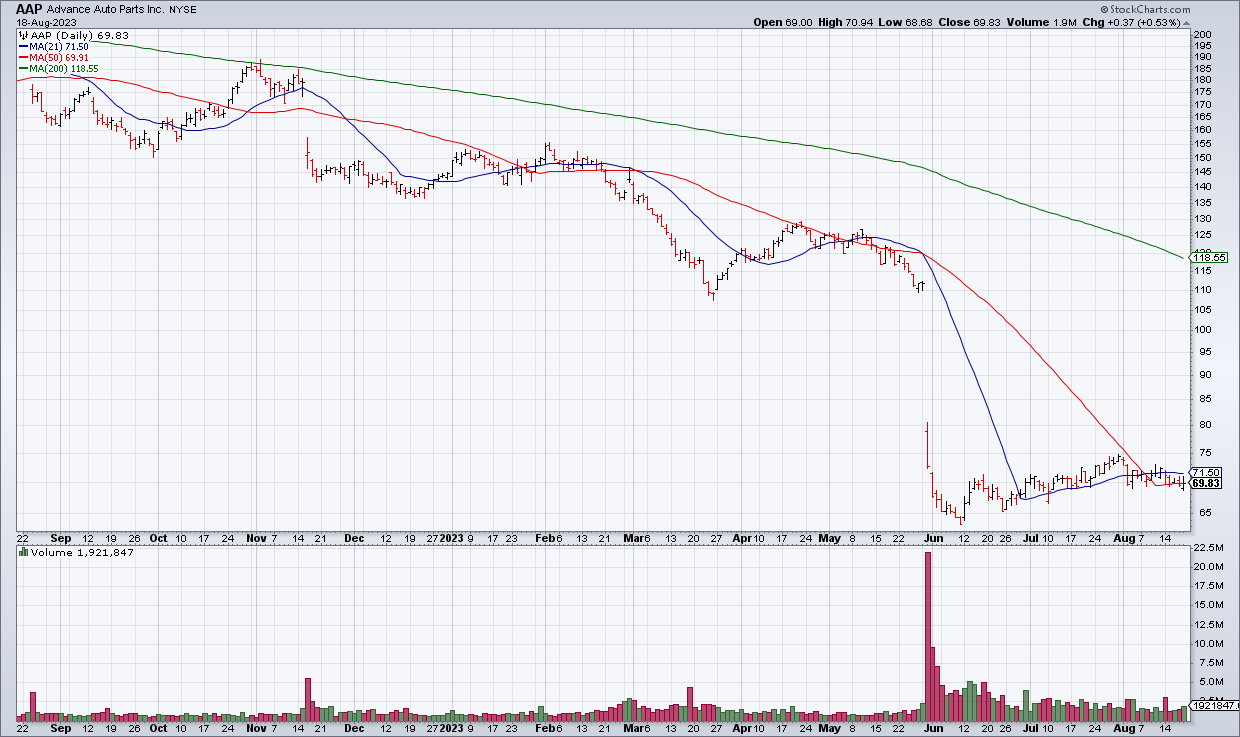

Next up: AAP. AAP operates more than 5,000 auto parts stores including almost 4,500 under the Advanced Auto Parts brand. While smaller and less well known than its competitors AutoZone (AZO) and O’Reilly (ORLY), that is still a significant footprint. Last quarter was a disaster for AAP. Weak results led to a drastic decrease in full year guidance. AAP reduced full year EPS guidance from $10.20-$11.20 to $6.00-$6.50 and cut its quarterly dividend from $1.50 to 25 cents. That sent the stock down by about a third on heavy volume – as you can see in the chart above – which got my attention. Obviously risk is heightened here but I picked up a small position and am interested to see how 2Q23 results shake out Wednesday morning.