Josh Brown: “Valuation Is Junk Science”, MJ: The Hangover, DIS Earnings

Note: To sign up to be alerted when the morning blog is posted to my website, enter your name and email in the box in the right hand corner titled “New Post Announcements”. That will add you to my AWeber list. Each email from AWeber has a link at the bottom to “Unsubscribe” making it easy to do so should you no longer wish to receive the emails.

The best lack all conviction, while the worst are full of passionate intensity – Yeats, “The Second Coming”

Yesterday afternoon when researching this note I came across an amazing CNBC Closing Bell interview from Wednesday afternoon with Josh Brown, the soon to be 44 year old CEO of well known, $1.3 billion AUM Ritholtz Wealth Management, also known as The Reformed Broker with 1.1 million Twitter followers. Josh is essentially the face of young Wall Street. He is the guy young investors listen to and the leader of the next generation of investment advisors. So when he speaks, it’s worth listening to. And he didn’t hold back Wednesday afternoon.

In the interview, Josh said that “Valuation is junk science” in the sense that it gives “no signal” as to what stocks are going to do over the next month, 3 months, 6 months, year, even 5 years. What matters now is “liquidity”. Clearly, this is the right interpretation of the present moment but there’s an investor in Omaha whose been doing this for more than 60 years and done okay espousing the exact opposite premise, namely, that valuation is an extremely important part of the investment process. In 1999, they wrote him off as out of touch and he gave a famous speech in Sun Valley about how things would turn out badly. Josh and the many investors rationalizing the current market are essentially writing him – and the investment philosophy that has made him one of the greatest investors of all time – off again.

At the 1:30 mark of the interview, Brown raises his voice and starts screaming: “People are like, ‘Well, ooh, valuations are high’. Well where should they be? You throw your dart, I’ll throw mine.” The last sentence is interesting. He’s referencing a famous study in which monkeys throwing darts at the stock tables in a newspaper did as well with the stocks their darts hit as professional investors who carefully picked their stocks. Are we all just throwing darts then? Have research and analysis become completely useless? To be fair, this was somewhat of a throwaway comment following upon the main point but I do think it was revealing.

Because the problem is that if we’re not going to use valuation as part of our stock selection process, how do we know when to buy and sell? Fundamentals can only get you so far. For example, Amazon (AMZN) is a great company with great fundamentals. Part of the reason is that it has the secular tailwind of the shift from brick and mortar to online spending by consumers at its tail. But that doesn’t mean it’s worth any price. Valuation helps us to understand if it’s worth $1000, $2000, $3000 or $5000. Josh’s alternative amounts to saying “Well, there’s a ton of liquidity in the system so just buy it no matter the price”. So now we’re advising investors to buy and hold the leading stocks regardless of valuation. A similar perspective was espoused about The Nifty Fifty in the 1970s. It was thought that they were “one decision” stocks: You just bought them and forgot about them because they’d never go down. It didn’t exactly work out that way.

This is a very important interview because it encapsulates the philosophy of the professional investment herd right now. Most professional investors know that valuations are high, if not extremely high, but due to career risk and Fear Of Missing Out (FOMO) they continue to stay invested. Unfortunately, this will end badly for their clients, just like it did in 2000 and just like it did in 1973. Fortunately for them, “Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally” (Keynes). That is, when this bubble does pop, all the professional investors will be caught and so each will be able to say “Everybody else got hit too” and hold onto their jobs.

It wouldn’t surprise me if “Valuation is junk science” goes down in history as the equivalent of Irving Fisher’s “Stocks appear to have reached a permanently high plateau” (1929) and Haslett and Glassman’s book Dow 36,000 (1999).

Yesterday morning (Thursday), I wrote about the incredible move in the marijuana stocks during the first three days of the week but that it had probably gone too far. That turned out to be a good call as the Marijuana ETF, MJ, had been +42% Monday through Wednesday but was -24.6% on greater than 7x average volume yesterday.

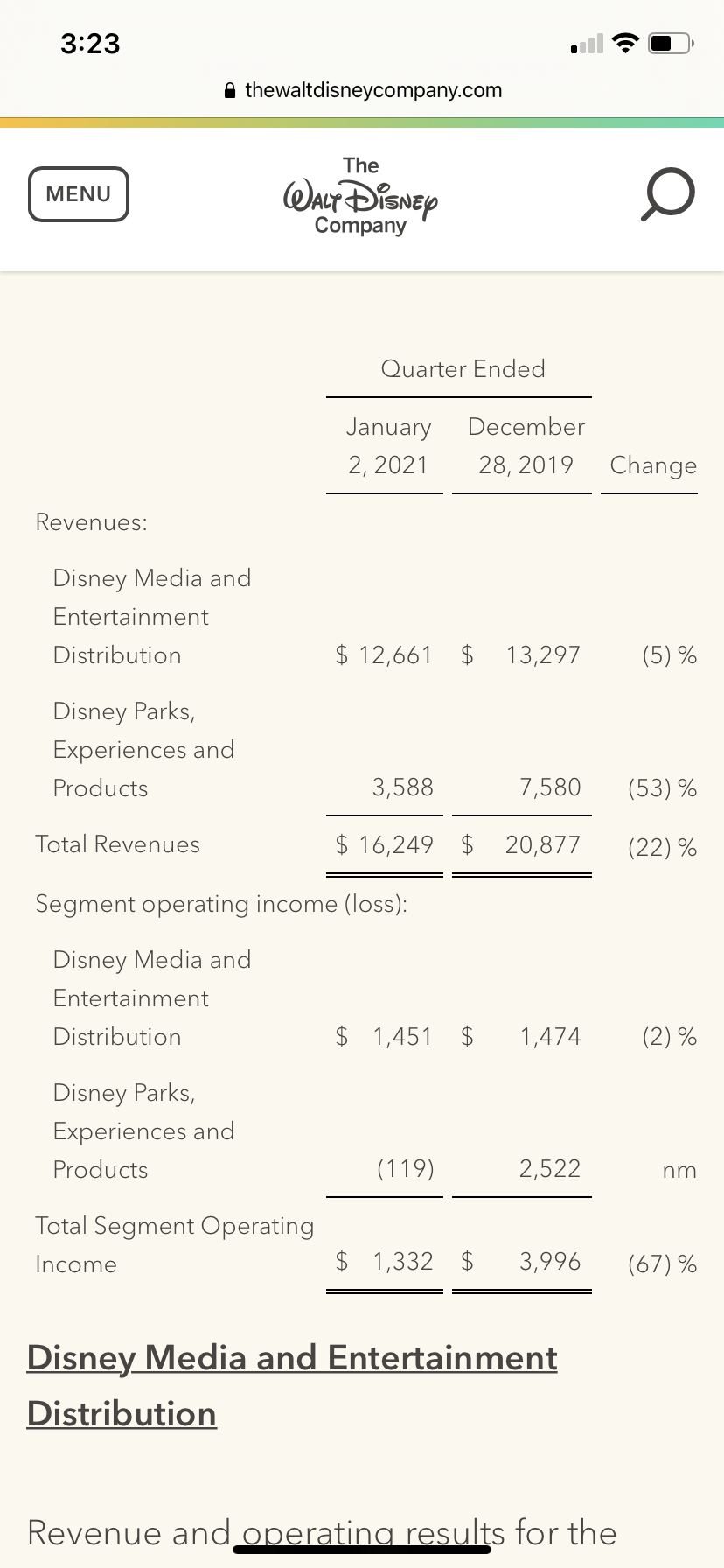

Lastly, I want to talk about Disney (DIS, market capitalization $353 billion) earnings from yesterday afternoon. DIS is a great and storied company but its Parks Segment is struggling during the pandemic. Yesterday afternoon, they reported a 53% decline in revenue and a $119 million 4Q20 loss in the segment. As far as the quarter, Parks overwhelmed a mediocre quarter from the company’s other segment, Media and Entertainment.

But investors are simply ignoring these parts of the business and focusing exclusively on the exponential subscriber growth of Disney+. It’s clear that investors view Disney+ as the next Netflix and are giving the rest of the business a free pass as a result. However, it is still very early innings for that business and it is not yet close to profitable. Regardless, DIS stock is up about 1% in the premarket to all time highs as I write.