Market Preview Week of Feb 27-Mar 3: KR TGT COST AZO Earnings

Next week a number of Top Gun holdings report earnings: Kroger (KR), Target (TGT), Costco (COST) and AutoZone (AZO).

Kroger (KR), Position Size: 6.27%, Market Cap: $32 Billion

KR – the leading grocery chain in the country – is one of Top Gun’s largest positions. My thesis is that as recession and inflation squeeze consumers, they will cut back on discretionary items but not necessities like groceries. Last quarter, KR guided full year Identical Sales growth to 5.1%-5.3% and Adjusted EPS to $4.05-$4.15. That works out to a PE of 11x current year earnings. KR also pays a 2.38% dividend. KR is one of the best stocks in the market to own right now in my opinion.

Target (TGT), Position Size: 1.56%, Market Cap: $77 Billion

TGT is one of the leading retailers in the country. While it’s mix of merchandise is more discretionary than KR or Top Gun holding Walmart (WMT), I still think TGT will maintain market share in a difficult economic environment. TGT is going through a rough patch and guided 4Q22 comps to a low single digit decline and operating margin to 3%. These are not great numbers but my thesis is that TGT is righting the ship and is in the process of turning things around. TGT earned $13.56 in 2021. Through the first nine months of 2022, TGT earned $4.12 – down 60%. But I think the earnings power is still there and TGT will realize it soon enough making shares a good value.

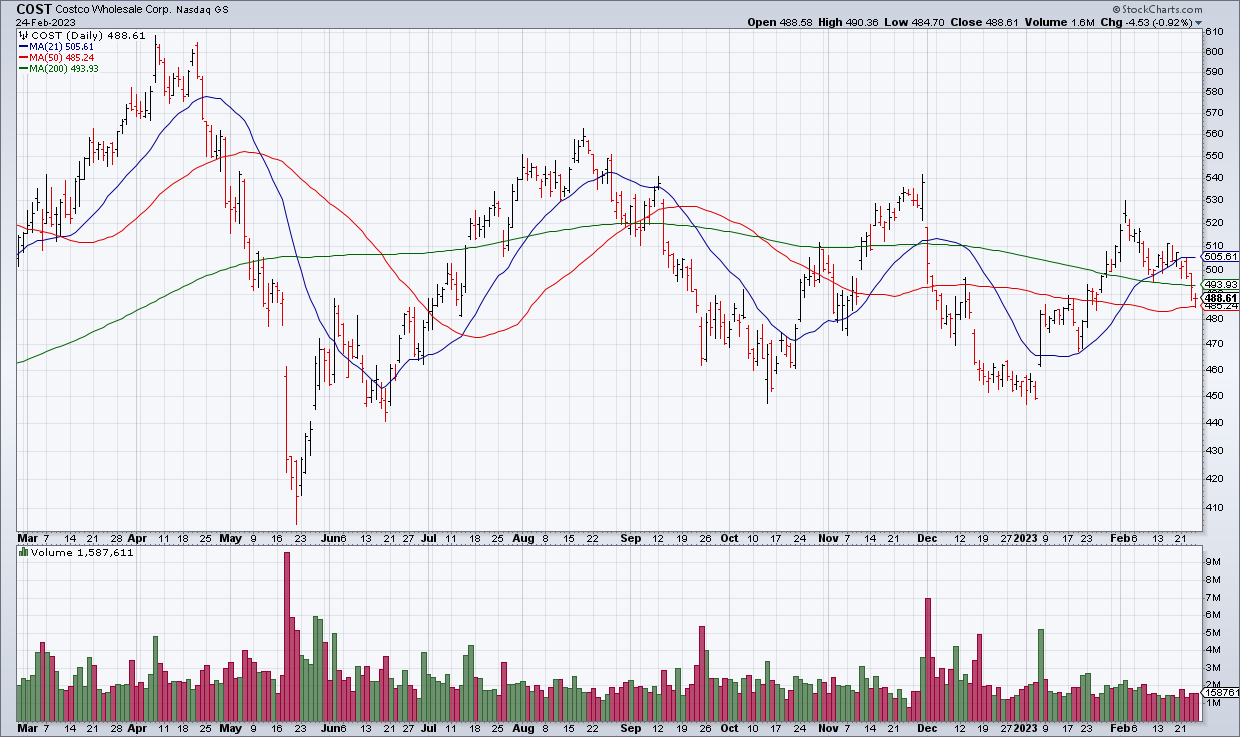

Costco (COST), Position Size: 0.91%, Market Cap: $217 Billion

COST is one of the greatest stocks of all time. It’s brand is synonymous with value. COST members are generally raving fans of the business. The thesis here is the same as KR: In a tough economic environment, consumers will be focused on necessities and value. That is COST’s sweet spot. The one caveat with COST is valuation. It trades at 33x my FY23 EPS estimate of $15. Sometimes you have to pay up for quality.

AutoZone (AZO), Position Size: 0.71%, Market Cap: $50 Billion

AZO is a leading auto parts retailer. My thesis here is that in a tough economic environment consumers will opt to repair their cars rather than purchase new ones. AZO trades at 21x my FY23 EPS estimate of $122.50. AZO is a high quality company and its stock has outperformed for decades.