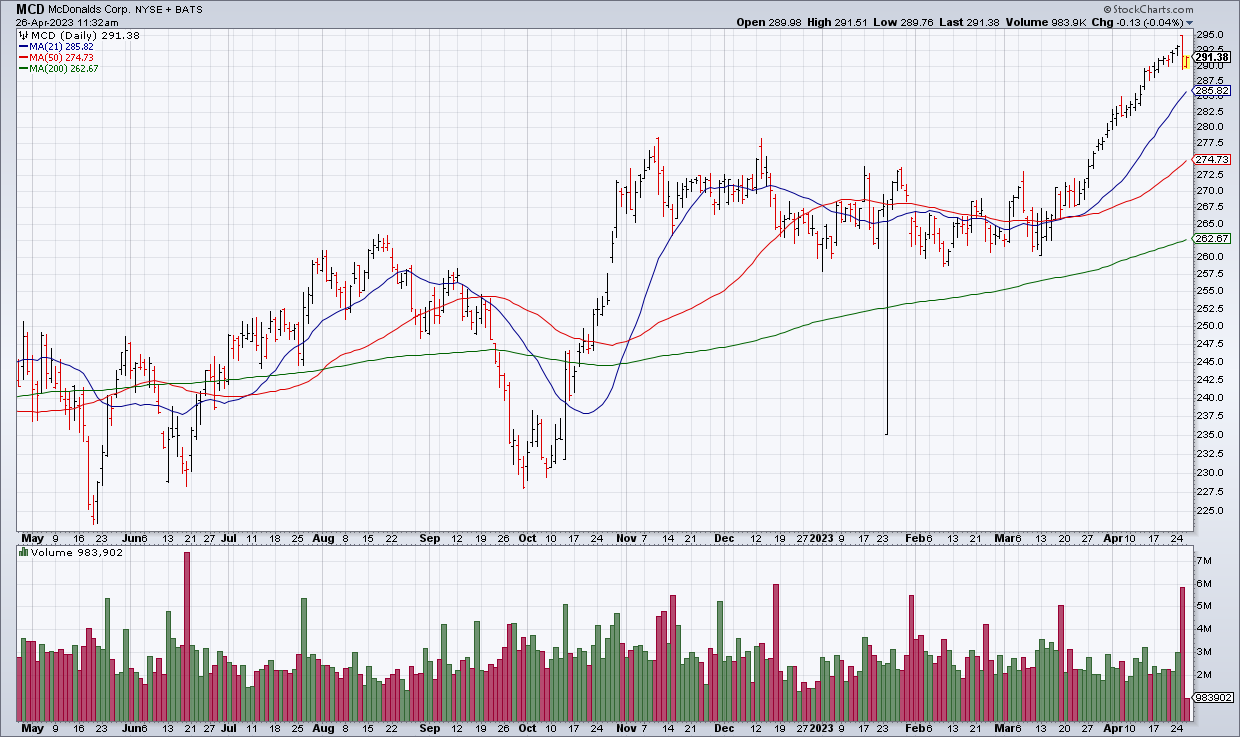

MCD For The Long Term

I believe that the middle class is thinning out and more and more this country is being divided into haves and have nots – and the have nots love eating at McDonald’s (MCD). This was borne out in MCD’s 1Q23 earnings report Tuesday morning.

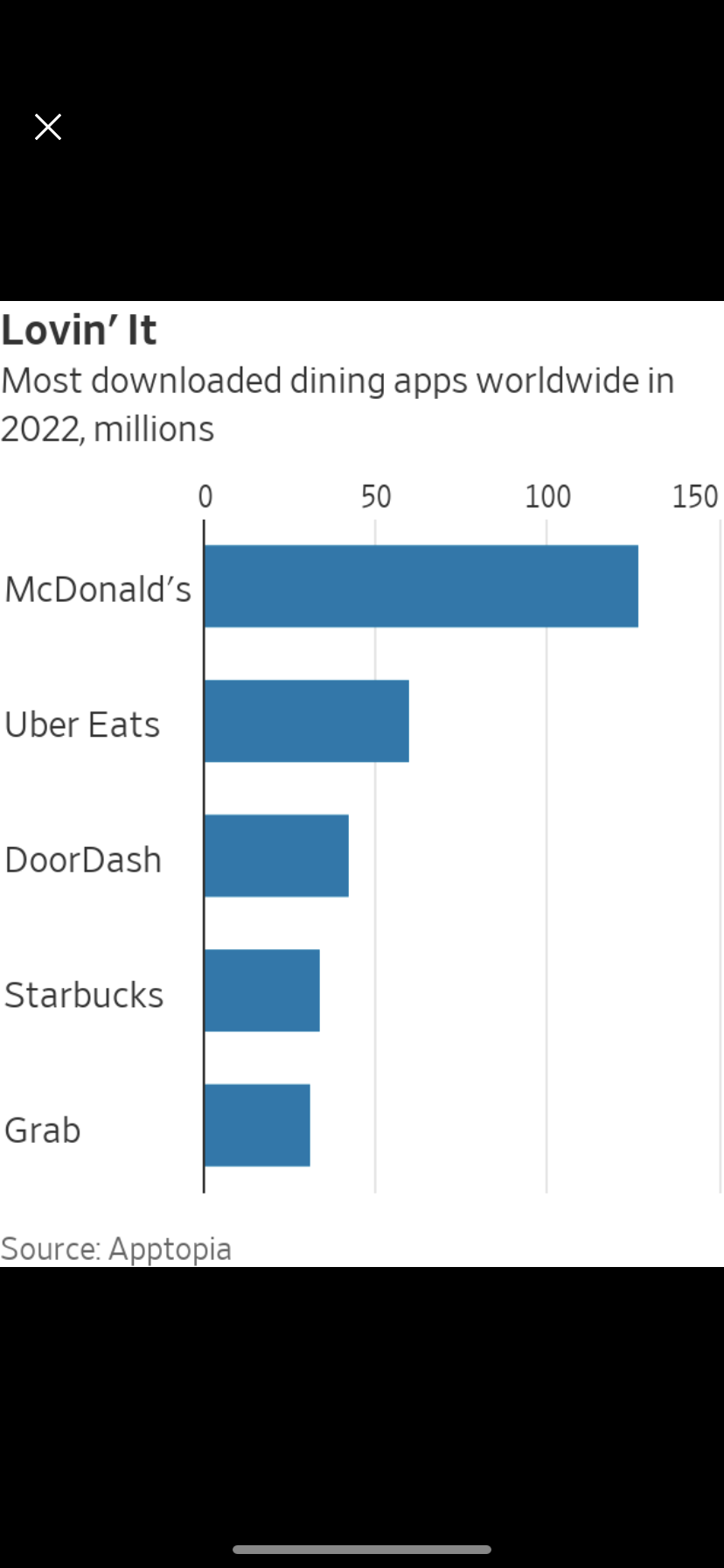

US comps were +12.6% – as were Total Comps. That’s a huge sales increase. Also impressive is that digital sales from its app were almost 40% of the total in its six largest markets – Spencer Jakab emphasized this in his column on MCD in this morning’s WSJ (“How McDonald’s Keeps Its Edge” [SUBSCRIPTION REQUIRED]). MCD is well integrated into the App Economy.

MCD’s EPS increased 15% to $2.63 which leads me to believe they can earn at least $11/share this year compared to $10.10 in 2022. That doesn’t mean the stock is cheap ($291 / $11 = 26.5x) but – as with Procter & Gamble, Coke and Pepsi – MCD is worth paying up for.