No Value In The Mega Caps

Mega caps – especially the Mag 7 – have driven the market indexes of late but it’s hard to justify further price increases because the stocks are more than fully valued at this stage. That’s not to say the market can’t go higher. The market can do anything. It’s simply to say that such a move is probably not justified or sustainable.

Let’s start with the most important stock in the market – Nvidia (NVDA) – which just reported 3Q earnings. It was another great quarter with revenue of $35.1 billion and EPS of 81 cents. 4Q guidance is for revenue of $37.5 billion. These are really big numbers.

The one weakness in the report was the 4Q guide for gross margins of 73.5%. Gross margins peaked at 78.9% in 1Q24 and have come down every quarter since then – and the guide suggests that will continue. I’m not sure what the reason for this is but it crimps NVDA’s profitability. This may be one of the reasons NVDA isn’t getting much pop in the after hours.

The problem with NVDA – and essentially all the mega caps – is valuation. Even if you think the AI boom will continue throughout all of next year and NVDA will earn something like $3.88 in 2025, the stock is still trading at nearly 40x that.

It’s well worth watching CNBC’s interview with Davidson’s Head of Technology Research Gil Luria that was done contemporaneously with the release of NVDA earnings. Davidson is one of the few analysts with a Hold rating on NVDA. In addition to valuation, Luria points out that unless the hyperscalers are getting a good return on their investment in NVDA chips for AI, they may cut back their high level of capital spending. In other words, the current boom in spending on NVDA’s chips may not last.

Crescat Capital made the same point in their investment letter from August 31: “It’s great for NVDA and its shareholders as long as the capital spending party is still raging, but what happens if NVDA’s customers are not getting a positive return on that investment? The party could be over and might even end in an economy-wide hangover.”

As I wrote on Saturday, overvaluation applies to mega caps outside of tech as well like one of my personal favorites and biggest winners, Walmart (WMT). While I love to see the 66% YTD gain in shares, the valuation has become bloated. WMT increased 2024 EPS guidance to $2.42-$2.47 when it reported earnings Tuesday morning. At today’s closing price of $87.18, that’s 36x – way too high.

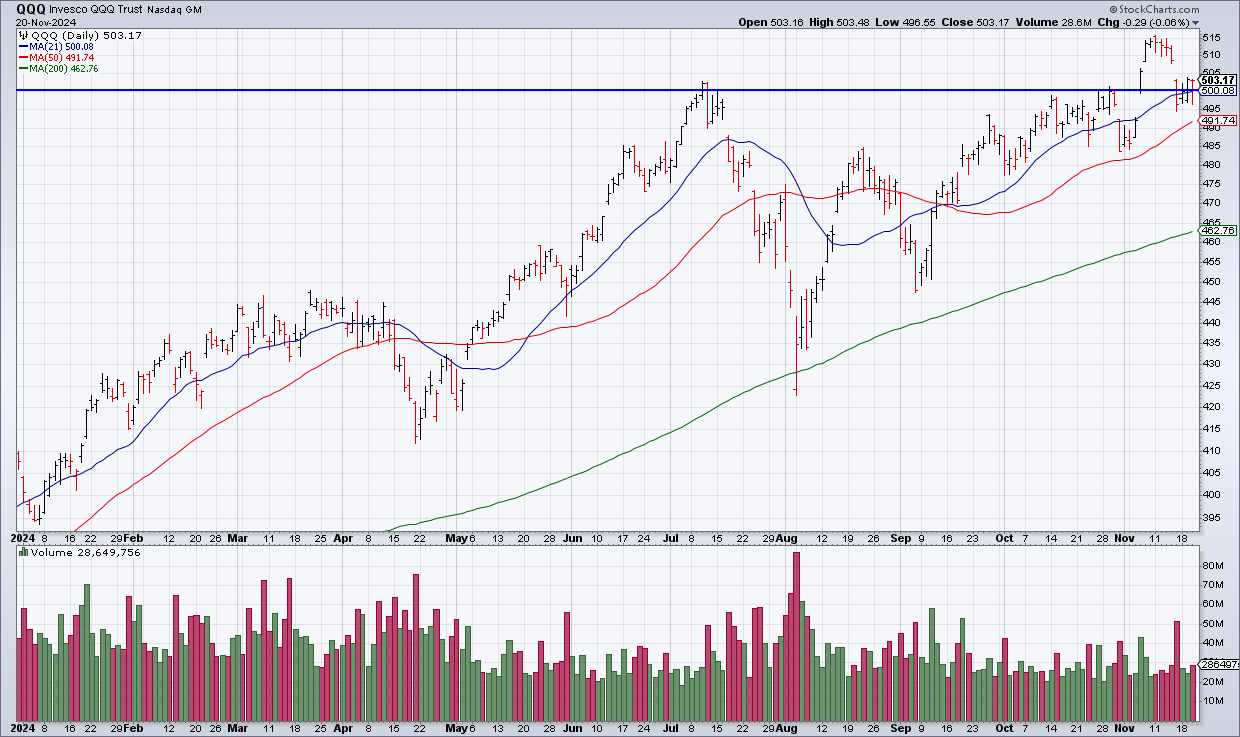

The most important three letters in the stock market for the last 15 years are QQQ. Had you trained a monkey to press those three letters, you would have outperformed the vast majority of active stock pickers and saved yourself a lot of time. $500 is an important level. QQQ has flirted with breaking out above it but hasn’t really been able to sustain a move.

Blackrock just launched an interesting ETF which tracks the Top 20 US stocks (TOPT). While it is weighted towards tech, it has other overvalued stocks like Costco (COST). This has been the right play for a long time but I wonder if we aren’t approaching an inflection point.