PYPL Is Ready

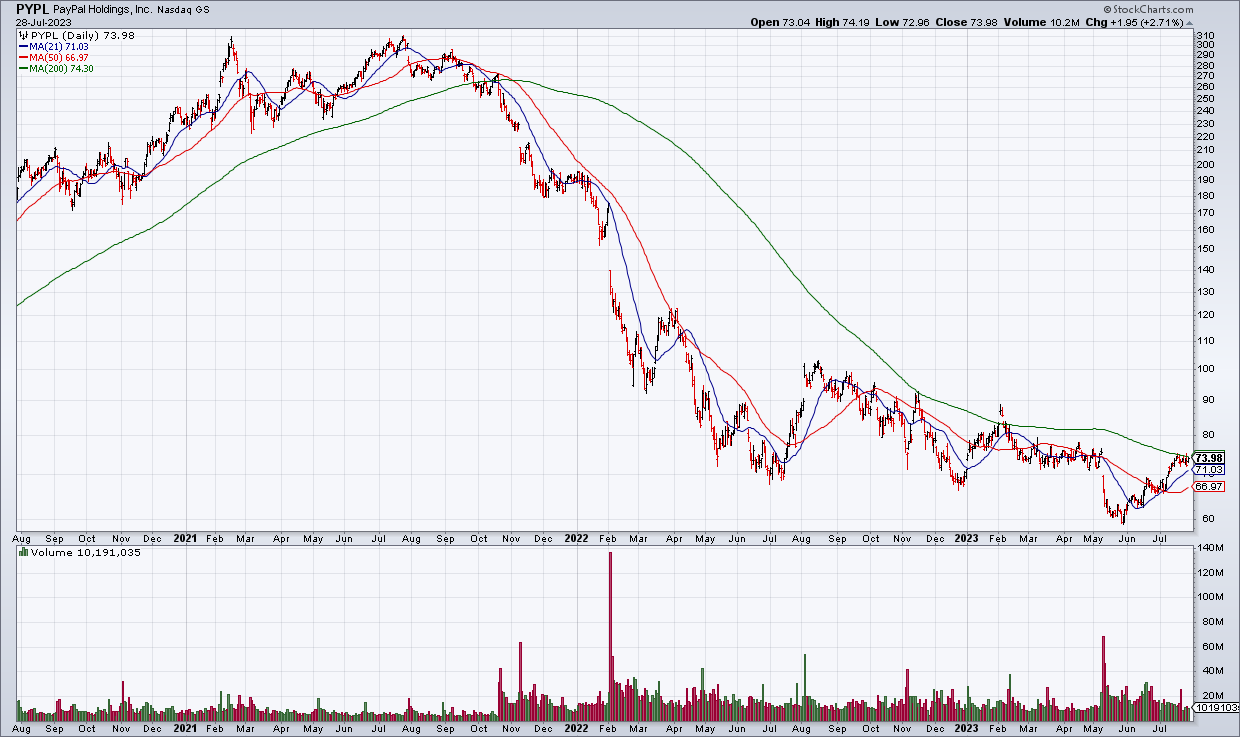

With stocks surging higher this year it’s hard to find real value in the market. One stock that is a screaming bargain – however – is PayPal (PYPL). Two years ago PYPL was loved and overvalued; today it’s hated and undervalued. And with the overall market moving higher – and the economy seemingly holding up in the face of all the Fed rate hikes – PYPL may be poised to play catch up.

I have been accumulating a position for the last 9 months and I think this could be the quarter that gets the stock going when they report 2Q23 earnings Wednesday afternoon. The bar is quite low with PYPL guiding 2Q23 revenue growth to 6.5%-7.0% and trading at 15x current year EPS guidance of $4.95. PYPL is doing the right thing by buying back close to 5% of its diluted share count this year at these depressed prices. In addition to shares, I may speculate on earnings with PYPL Aug4 $80 Calls which closed Friday at $1.12. There’s not a lot of value in this market right now but PYPL is a notable exception.

Disclosure: Top Gun is long shares of PayPal (PYPL).