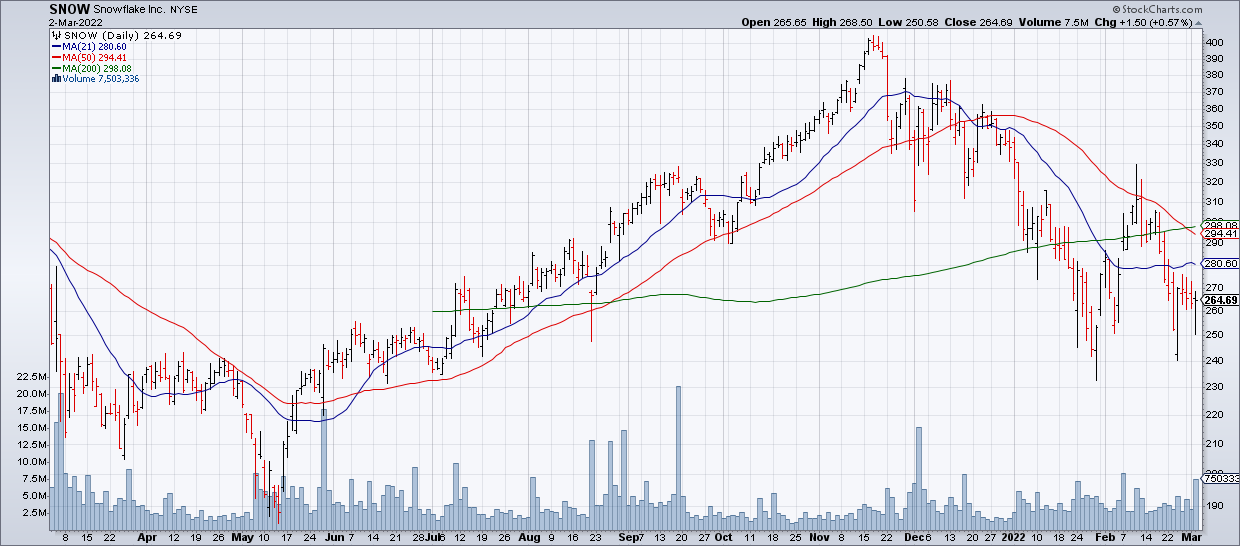

SNOW Is Melting

Cloud data platform Snowflake (SNOW) reported 4Q21 earnings after the close Wednesday. Revenue of $384 million was +101% year over year and they had $18 million in operating income. SNOW guided 2022 revenue to $1.88 billion to $1.9 billion (+65% to +67% compared to 2021) and operating margin to 1%. However, the stock is down ~20% in the premarket Thursday.

Why is SNOW melting? SNOW may well provide a great data analytics platform but it’s exactly the kind of expensive, early stage, cloud software stock that is out of favor right now. Even at its current after hours price, SNOW still trades at more than 30x its 2022 revenue guidance. Significant profitability is years away.

While I have been buying some these former high flyers, I’m not ready to buy SNOW. Why? The former highfliers I’ve been buying are down 70%-80% from their highs while at its current premarket price SNOW will still be down less than 50% – though this could change in the cash session. If the great growth investor Puru Saxena likes SNOW, it’s probably a great company and there will be a time to buy it but this isn’t capitulation yet in my opinion.