The Brutal Economics of Food Delivery: The Case of DASH

Note: To sign up to be alerted when the morning blog is posted to my website, enter your name and email in the box in the right hand corner titled “New Post Announcements”. That will add you to my AWeber list. Each email from AWeber has a link at the bottom to “Unsubscribe” making it easy to do so should you no longer wish to receive the emails.

Food-delivery companies did record-breaking business during the pandemic, as millions of homebound Americans embraced the idea of ordering dinner via smartphone apps. Their valuations skyrocketed. They acquired reams of data that helped increase their efficiency. There was just one problem: Even at the height of their success, they weren’t making any money.

Now, as the pandemic wanes, companies like DoorDash Inc., Uber Technologies Inc and Grubhub Inc. are trying to address what could be a life-or-death question: How can they make the math work?

“You really need to optimize things to the cent,” said Pierre-Dmitri Gore-Coty, the global chief of Uber’s delivery business, which includes Uber Eats..

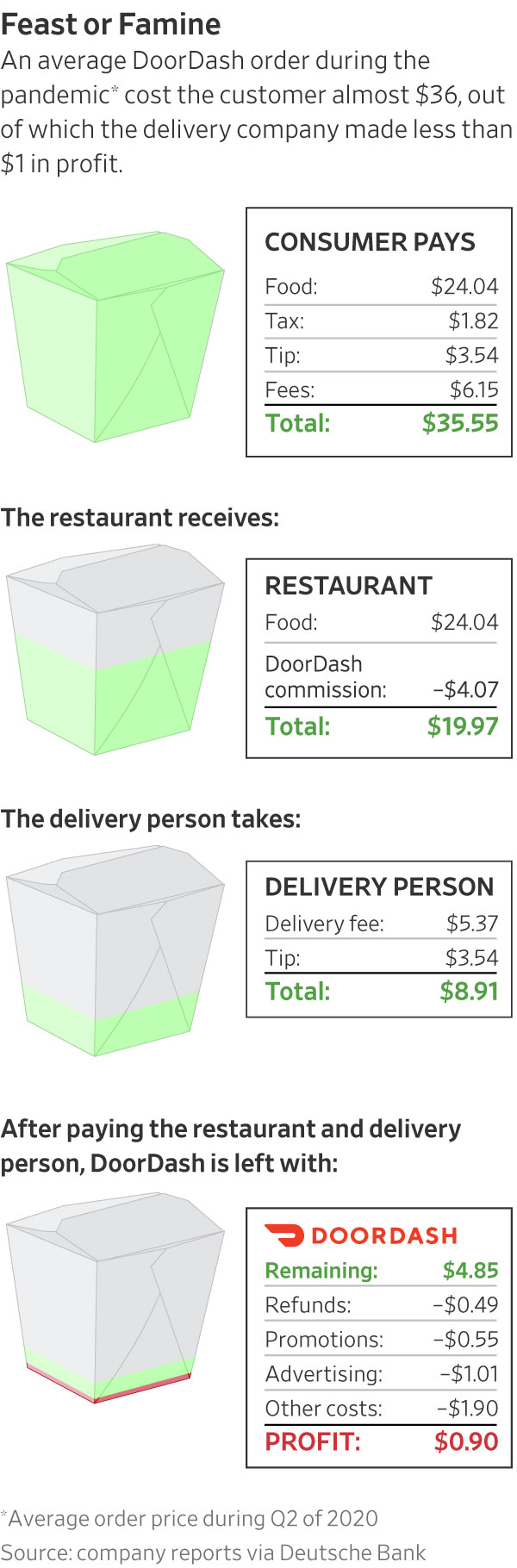

Delivering food is an expensive logistical undertaking. Apps earn money by charting restaurants a percentage of the order, as well as by charging customers a service fee. They then dip into those earnings to pay drivers, their biggest expense.

After accounting for advertising costs and refunds to customers, among other operational expenses, DoorDash on average is left with 2.5% of a customer’s overall bill, accordin to a Deutsche Bank analysis. That means DoorDash ended up with 90 cents on the average order during the height of the pandemic, worth around $36 – Preetika Rana and Heather Haddon, “The Race To Make Food Delivery Pay” [SUBSCRIPTION REQUIRED], WSJ, May 29

Almost a decade ago, when DoorDash (DASH) was just getting started, I needed money and took a temp job at their small headquarters at the corner of Page Mill Road and El Camino in Palo Alto, CA. My job was to call local restaurants to get their hours for an upcoming holiday and enter that information into a spreadsheet. It was mind numbing work and it didn’t pay much.

Prior to the pandemic, things came full circle as I became a regular customer and ultimately subscriber to DASH’s food delivery service. (I cancelled my subscription during the pandemic due to concerns about drivers and COVID).

On December 9, 2020, DASH shares began trading on The New York Stock Exchange and closed yesterday (Wednesday June 2) with a market capitalization of $49 billion.

Unfortunately for DASH and the other players in the food delivery space like Uber and Grubhub, the economics of food delivery are terrible. “[It] is and always will be a crummy business”, Grubhub CEO Matt Maloney told the WSJ. (Grubhub is getting out of the food delivery business).

As you can see from the above graphic, on an average order of $35.55 during the height of the pandemic, DASH only made 90 cents.

Three weeks ago on Thursday afternoon May 13, DASH reported 1Q21 earnings. They guided Gross Order Volume to $35-$38 billion and Adjusted EBITDA to $0-$300 million. In other words, DASH expects to deliver more than $35 billion worth of food this year and barely make any money even excluding stock based compensation and depreciation and amortization.

If DASH can’t make money delivering more than $35 billion worth of food, what makes one think it can at $100 billion? While DASH offers a convenient service for consumers, from a business standpoint the economics may not make sense.