The Return of Value?, Breaking My Value Trap Habit / Mark Minervini on Leaders vs Laggards, Integrating Not Imitating Minervini

Note: A few months ago I started writing a daily morning market email for clients, friends and family. I recently decided to start making this email more broadly available. Email me at gfeirman@topgunfp.com if you’d like to be added to the list.

It’s early but the Futures are up with the S&P Futures +0.75%, NASDAQ-100 Futures +0.45% and the Russell Futures +1.1% as of 2:48am PST. If those levels hold into the open, we will move into the upper range established by David Zarling’s “Dueling Tails” from last Monday (3,646) and Tuesday (3,512)(I included Zarling’s chart enough in last week’s emails. Email me if you need a copy).

We are on the cusp of a sustained rally in value. This rotation has room to continue much further, given the material underperformance we have witnessed in recent years – JP Morgan Strategists Davide Silvestrini and Marko Kolanovic, quoted in Andrew Bary, “A Covid Vaccine is Coming. Here’s What It Means for the Stock Market”, Barron’s, 11/14/20

The price-to-book ratio of the Russell 1000 Growth Index trades at more than five times that of value, and the forward price-to-earnings ratio is close to twice as high, the biggest premium for growth since the dot-com bubble of 2000. Growth has beaten value for 14 years, the longest period since data from Prof. Kenneth French at Dartmouth’s Tuck School of Business started in 1926…. This year through September, value fell behind growth by the most of any full year in the data, so there is a lot that could be reversed – James Mackintosh, “Value Shares Receive A Shot in the Arm”, WSJ, 11/13/20

The biggest story since the announcement of the vaccine on Monday morning continues to be the #Rotation from #StayAtHome #PandemicBenificiary stocks into #ReOpen #RealEconomy stocks. This maps pretty decently onto growth vs value. In other words, last week, especially Monday and Tuesday, we have seen a ferocious reversal in value over growth as investors try to price in a #ReOpen based on the vaccine. As a value investor, this reversal has been a long time in the making and I’d love for it to be sustained this time, rather than one of the many false starts we’ve had over the last decade and a half.

Getting the trading stuff out of the way, it’s another slow earnings week though Walmart (WMT), Home Depot (HD) and Nvidia (NVDA), each large, important companies, report.

Like I said last week, as long as we continue to trade within Zarling’s “Dueling Tails” and are aware of this #Rotation from #Growth into #Value we should have a pretty good handle on the key things to watch during the trading day, which gives us an opportunity to step back and talk about some bigger picture issues which I am going to do now.

I have a bad habit. No: I’m not a drinker or a smoker nor do I eat a lot of sweets. Rather I have long been addicted to #ValueTraps, low P/E stocks that look cheap but are so for a reason. I’m in good company here as Warren Buffett had the same bad habit early in his career:

It must be noted that your Chairman, always a quick study, required only 20 years to recognize how important it was to buy good businesses. In the interim, I searched for “bargains” – and had the misfortune to find some. My punishment was an education in the economics of short-line farm implement manufacturers, third-place department stores, and New England textile manufacturers [obviously a reference to Berkshire Hathaway itself in its original form](1987 Letter to Shareholders)

Eventually, Buffett learned his lesson and the rest is history:

It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price. Charlie understood this early; I was a slow learner. But now, when buying companies or common stocks, we look for first-class businesses accompanied by first-class managements (1989 Letter to Shareholders)

(For those of you who want to learn more about Buffett’s evolution from a Graham deep value style investor to a Phil Fisher quality value investor, the best resource is Chapter 2, “The Two Wise Men”, of Robert Hagstrom’s The Warren Buffett Way).

Alright: Enough about this Warren Buffett guy. Let’s talk about me!

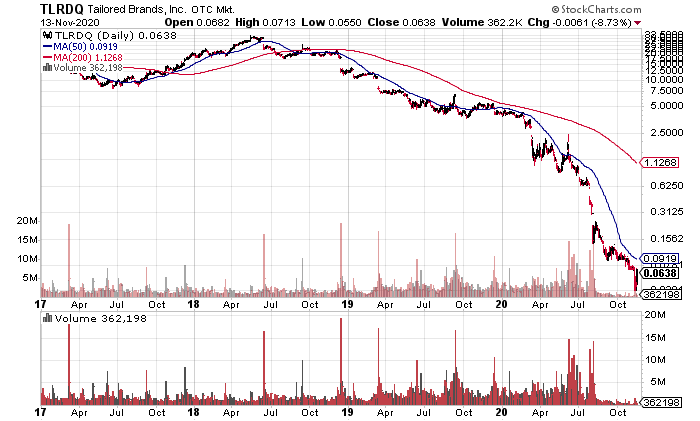

A failed trade in value trap Tailored Brands (TLRDQ) from January 2019 through March 2020 awoke me from my “dogmatic slumber” (Kant re: Hume on causality, The Critique of Pure Reason). I bought a small position in the stock at $12 in January of 2019, added by two-thirds in March 2019, again at $12, and rode it down to $1.34 before selling in March 2020. The stock has been delisted from the NYSE, trades on the pink sheets, and closed Friday at 6 cents. It was a terrible investment based on a mistake I’ve made many times in the past that hurt my ego. But I finally learned my lesson: No more #ValueTraps; buy #HighQuality companies.

This was further driven home to me by Mark Minervini’s Master Trader Program, the first half of which I completed this past weekend. Mark breaks stocks down into 6 categories, the first of which is Market Leaders and the last of which is Laggards. #ValueTraps are a significant subset of #Laggards Laggards lag and I’m sick and tired of buying underperforming stocks.

To have lasting success in the stock market, you must decide once and for all that it’s more important to make money than to be right. Your ego must take a backseat – Mark Minervini, Trade Like A Stock Market Wizard (290)

The other thing that I have had reinforced for me from Minervin’s Master Trader Program, this time entirely from my preparation not the course itself as we won’t cover Risk Management until next Sunday, is #RiskManagement I failed to manage risk with TLRD and I recently failed to manage risk in a short campaign that lasted from May through September. I let our shorts move against me far too much, costing me and my margin account clients a significant amount of money, by not practicing good risk management. Again, this isn’t the first time I’ve been stubborn and made this mistake. It’s time to put an end to this as well and practice tighter, disciplined, risk management. I’m not exactly sure what that’s going to look like but I’m actively working it out.

I must create a system or be enslaved by another man’s – William Blake

One repays a teacher badly if one remains always only a pupil – Nietzsche

To some people, it’s bad marketing for me to reveal that I’m taking Minervini’s course because it shows that I’m still learning and don’t have it all figured out. To those people I say: We should all still be learning in this game; nobody has it all figured out. I’m constantly trying to add pieces to my game and improve and I’m not ashamed to admit that my game has holes and that I can get better.

However, it is important to note that I do not intend to become a Mark Minervini clone, or anyone else’s clone for that matter. My process is to take from all the greats who have come before me what makes sense to me and integrate it into my own system, which also includes my own original contributions.

With respect to Minervini, technical criteria come first for him and, while a “techno-fundamentalist” like me, he leans more technical than fundamental. I will likely continue to lean more in the opposite direction. It’s just what makes sense to me and better suits my personality.

As far as risk management, Mark is simply right and I need to significantly step up my game. Mark devotes the last two chapters of his book to risk management and we will be covering it in the Master Trader Program all day Sunday, November 22. I will continue to be working out a system of risk management that makes sense to me and prevents the kind of debacles I experienced with TLRD and this year’s shorting campaign.

The biggest difference between Mark and I is and will remain Macro. Macro is the biggest part of my process and plays no role in Mark’s (or Buffett’s) system. I believe that Macro has been the driving force in markets for many years and that this will become even more so in the years ahead.

Nevertheless, we’re going to take the great insights Mark has to offer and we’re going to #GetBetter