NOTE: Every week I write a Client Note for my clients. For a limited time, I am allowing non-clients to sign up and receive the Client Note. You can sign up at the top right hand corner of the website. I will also be posting the notes on my blog with a 24-48 hour delay from time to time. Here is this week’s.

*****

By the weekend, all the pressure and threats and bribes had left the speaker three to five votes short. Her remaining roadblock was those pro-life members who’d boxed themselves in on abortion, saying they would vote against the Senate bill unless it barred public funding of abortion. Mrs. Pelosi’s first instinct was to go around this bloc, getting the votes elsewhere. She couldn’t.

Into Saturday night, Michigan’s Bart Stupak and Mrs. Pelosi wrangled over options. The stalemate? Any change that gave Mr. Stupak what he wanted in law would lose votes from pro-choice members. The solution? Remove it from Congress altogether, having the president instead sign a meaningless executive order affirming that no public money should go to pay for abortions.

The order won’t change the Senate legal language–as pro-choice Democrats publicly crowed within minutes of the Stupak deal. Executive orders can be changed or eliminated on a whim. Pro-life groups condemned the order as the vote-getting ruse it was. Nevertheless, Mr. Stupak and several of his colleagues voted yes, paving the way to Mrs. Pelosi’s final vote tally of 219.

Universal health care has long been a holy grail for liberals and on Tuesday they made history when President Obama signed a new health care bill into law.

The story begins on Christmas Eve last year when the Senate passed a bill 60-39 along strictly partisan lines (Kentucky Republican Jim Bunning did not vote). Unfortunately, the bill had a number of repugnant features, such as a special deal for Nebraska, a Cadillac tax on premium health insurance plans opposed by unions, and federal funding for abortions opposed by pro-life Democrats, among others. It soon became apparent that the Senate bill would not pass in the House.

Normally, the Senate would have fixed the bill and passed a new and improved version. But the election of Scott Brown to Ted Kennedy’s seat on January 19th made it impossible for Senate Democrats to pass a new health bill without Republican support. Democrats were now stuck with the politically toxic Senate bill and it appeared that health care reform was dead.

However, Democratic leaders decided to push ahead utilizing a new strategy. They would pass the Senate Bill and a bill of amendments to it in the House. They would then argue that the new amendments were not substantial revisions to the original Senate bill and could be passed under reconciliation rules in the Senate, requiring only a strict majority rather than 60 votes. Whether the amendments to the bill really fall under reconciliation is a thorny issue. Democrats avoided facing it by refusing to meet with Republicans and the Senate parliamentarian before the vote on Sunday.

On Sunday, the House passed the Senate bill 219-212 along strict partisan lines – not a single republican voted for the bill – and the amendments bill. The close vote shows that it was in doubt to the very end. Only a last minute agreement to issue an Executive Order banning the use of public funds for abortions persuaded Michigan Democrat Bart Stupak and his cohorts to vote Yes.

The close vote and frenzied last minute meetings and deals show that the bill did not enjoy broad support even in Congress. The Democrats rammed the bill through, circumventing the election of Scott Brown and resorting to reconciliation, without a single Republican vote in the Senate or House.

*****

On Thursday, the Congressional Budget Office reported that, if enacted, the latest health care reform legislation would, over the next 10 years, cost about $950 billion, but because it would raise some revenues and lower some costs, it would also lower federal deficits by $138 billion. In other words, a bill that would set up two new entitlement spending programs — health insurance subsidies and long-term health care benefits — would actually improve the nation’s bottom line.

Could this really be true? How can the budget office give a green light to a bill that commits the federal government to spending nearly $1 trillion more over the next 10 years?

The answer, unfortunately, is that the budget office is required to take written legislation at face value and not second-guess the plausibility of what it is handed. So fantasy in, fantasy out.

In reality, if you strip out all the gimmicks and budgetary games and rework the calculus, a wholly different picture emerges: The health care reform legislation would raise, not lower, federal deficits, by $562 billion.

The bill was signed into law by President Obama Tuesday and it is indeed a “big f-&%$-ing deal” as Vice President Biden whispered to Obama at the press conference oblivious that a nearby microphone picked up his comments. It is one of the biggest pieces of social legislation passed in the last 40 years and of a piece with Social Security (1935) and Medicare (1965).

The bill dramatically expands Medicaid, a free federal-state health care plan for the poor, adding 16 million to its rolls. It will also provide subsidies to another 19 million lower earning Americans for the purchase of health care on state run marketplaces. It essentially provides free health care for the poor and subsidies for the middle class.

There are also a variety of new controls and fees on health insurance companies.

The bill will be partly financed by removing the income cap on Medicare taxes and a new 3.8% Medicare tax on investment income for individuals earning more than $200,000/year and families earning more than $250,000/year.

The expansion of Medicaid and the subsidies will take effect beginning in 2014 and the new taxes on the wealthy will take effect starting in 2013. Some of the new restrictions and controls and health insurance companies will begin in the next few months.

The Congressional Budget Office (CBO) on Thursday said that the bill will lower federal deficits by $138 billion over the next 10 years, giving cover to Democrats claiming that passage of the bill is fiscally responsible. But such calculations are almost beyond belief.

As former CBO Director Douglas Holtz-Eakin wrote in Sunday’s New York Times (“The Real Arithmetic of Health Care Reform”, The New York Times, March 20), the CBOs analysis depends on leaving out $114 billion in additional spending that future Congresses would need to vote for, $53 billion in higher Social Security taxes the bill is supposed to result in by lowering company health care costs and thereby increasing wages, and $463 billion in Medicare cuts that nobody believes will happen. Accounting for hidden costs and gimmicks, Holt-Eakin estimates the bill will actually result in $562 billion in additional deficits over the next 10 years.

Even that number is probably an underestimate as the CBO estimated that ObamaCare will cost $200 billion a year when fully implemented and grow 8% per year thereafter.

The substantially increased government bureaucracy will suck efficiency, innovation and energy out of the American health care system. We can expect to see choice and the quality of care decline and the rationing of health care by waiting as in other public health care systems such as Canada and Britain.

*****

SPECIAL OFFER – FREE INVESTMENT REVIEW: For a limited time I am offering a free investment review. Pick any stock, bond, ETF or mutual fund. I will do a comprehensive fundamental/macro/technical analysis, write a concise analyst report, and consult with you for 30 minutes by phone or in person for free.

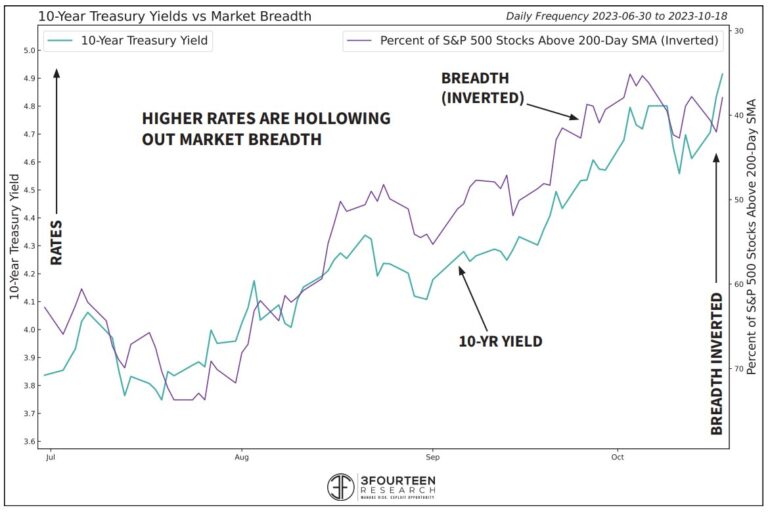

Fed Chair Powell sent interest rates soaring and tanked the stock market Thursday when he continued to press his “higher for longer” narrative at the Economic Club of New York. He doesn’t seem to understand that it’s time to change…

As we all know, the housing market is driving everything in this bust. And the financials, as the source of all the financing for the housing market, have borne the brunt of the pain and have led the entire stock…

You know Wall Street couldn’t go more than a few weeks without obsessing about the Fed and if there is going to be a rate cut this year or not. I swear to God…… The immediate cause is today’s April…

“The January retail sales data is not consistent with either same store chain sales or total vehicle sales during the sampling period.” – Joseph Brusuelas, IDEAglobal The surface rationale for today’s move is a stronger than expected January Retail Sales…

Sooner or later in a bear market, even the glory stocks start to come apart. As a bull market ages and becomes a bear market, stock groups turn down one by one, until even the strongest roll over. That may…

“The new capital will enable Fannie Mae to maintain a strong, conservative balance sheet….” – Fannie Mae 1st Quarter Earnings Release The Heard On The Street column in today’s WSJ, “Will $6 Billion Do For Fannie?” (subscription required), caught my attention. Fannie announced…