The Great Disconnect and The Fed Put

Everyone can see and feel that this is different and can sense the bizarre nature of the market response: we are in the top 10% of historical price earnings ratios for the S&P on prior earnings and simultaneously are in the worst 10% of economic situations, arguably even the worst 1%! – Jeremy Grantham, GMO 1Q20 Letter (https://www.gmo.com/americas/research-library/1q-2020-gmo-quarterly-letter/)

There were three notable earnings reports this week and each of them confirmed the insane disconnect between the real economy and the financial markets. On Wednesday afternoon, KB Homes (KBH) reported earnings for the quarter ended 5/31/20. New orders were down 57% for the quarter and while the stock dropped 12% today, it is still only 25% off its bull market highs. This morning (Thursday), Darden Restaurants (DRI) reported earnings for the quarter ended 5/31/20. The most significant data point from the report, in my opinion, is that comps for the first three weeks of June, through Sunday 6/21, were -33.2%. While it makes no sense to me, the stock jumped almost 5% and is up more than 100% from its March lows. Finally, Nike (NKE) reported earnings for the quarter ended 5/31/20 after the close today (Thursday). Revenues were down 38% and they lost 51 cents per share. The stock finished the after hours down 4% but is still only $8 off its all-time highs!

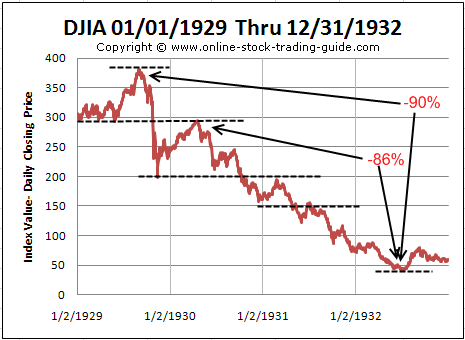

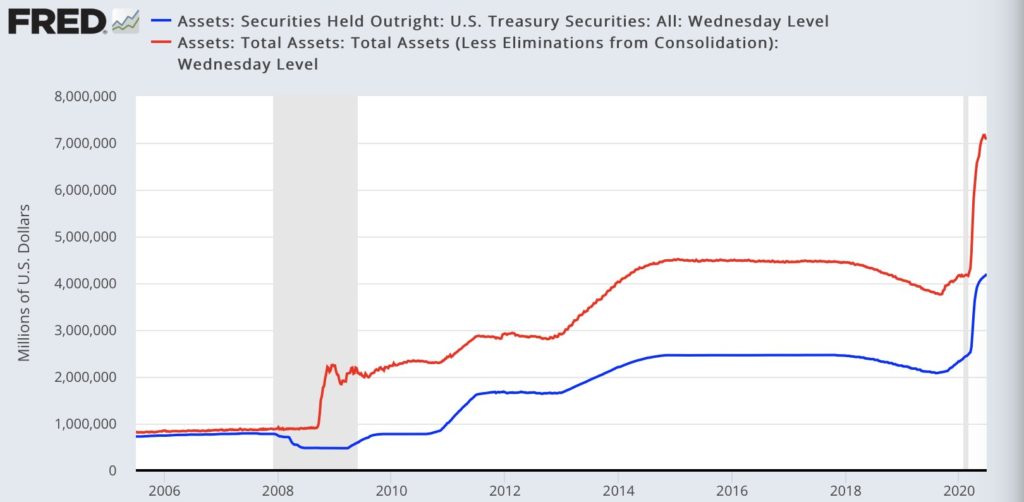

The main cause of this disconnect between the real economy and financial markets is the massive injections of liquidity by the Fed. In an excellent piece from Tuesday (https://www.fidelity.com/learning-center/trading-investing/markets-sectors/market-rally-2020?ccsource=email_weekly), Fidelity’s Jurrien Timmer, Director of Global Macro, argued that this is why the current rally, while similar to the one from 11/13/29 to 4/17/30, is unlikely to be a bear market rally in a Second Great Depression: “Because of support from the Fed, I don’t see a repeat of the 1930s happening today.”

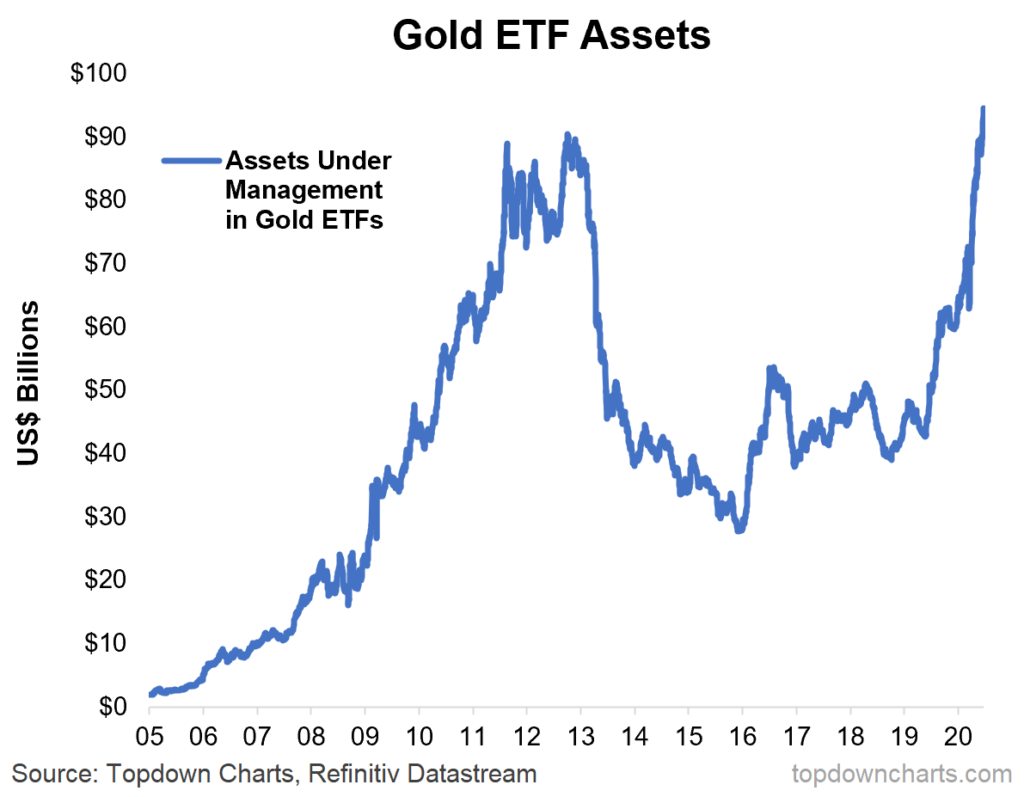

Timmer makes an excellent point that the policy response today is vastly bigger than the one at the onset of the Great Depression. However, he fails to ask the next question: What are the potential unintended consequences of such a massive and unprecedented injection of liquidity by the Fed? You don’t just inject $3 trillion into financial markets and the real economy (via loans to real companies) in three months without consequences. There are two that standout to me as highly likely. The first is the creation of asset bubbles. It is my firm conviction that the stock, bond and commercial real estate markets are all in enormous asset bubbles. The second is inflation. While most of the Fed’s money is going into financial markets, a significant chunk is being loaned to real companies who can spend it in the real economy, which could cause inflation. It’s no surprise that gold is testing $1800/ounce and investors are piling into gold ETFs.

For these reasons, I disagree with Timmer that this is not a bear market rally. The Fed’s injections have massively distorted financial markets and caused extreme bullish psychology. However, that is not the foundation for a genuine bull market in which previous excesses have been cleansed from the system, valuations are cheap and the stage is set for innovation and productivity growth. The great disconnect clearly shows that the stock market rally is artificial and it is my belief that unintended consequences will emerge shortly that will derail it.

Greg Feirman

Founder & CEO

Top Gun Financial (www.topgunfp.com)

A Registered Investment Advisor

P.O. Box 837, San Carlos, CA 94070

(916) 224-0113